What Are Real-World Assets (RWAs)? A Beginner-to-Pro Framework for 2025

How Traditional Assets Go Digital: Unlocking the Potential of RWAs in Crypto.

")

Real-World Assets (RWAs) are traditional finance assets—treasuries, bonds, real estate—tokenized on blockchain, enabling faster settlement, greater access, and new yield paths. RWAs are projected to hit $30 billion by 2026. They reduce costs, improve liquidity, and bridge the gap between crypto and legacy finance, but also carry risks around regulation, liquidity, and technical faults. Start small with stablecoins and tokenized treasuries, secure assets smartly, and gradually step into more advanced RWAs.

Why Real-World Assets Matter in Crypto

The next wave of digital finance is not just DeFi or NFTs. It is real-world assets, treasuries, bonds, and real estate, represented digitally on blockchains. These assets, known as RWAs, bridge the gap between traditional finance and crypto by allowing faster settlement, broader access, and new yield opportunities.

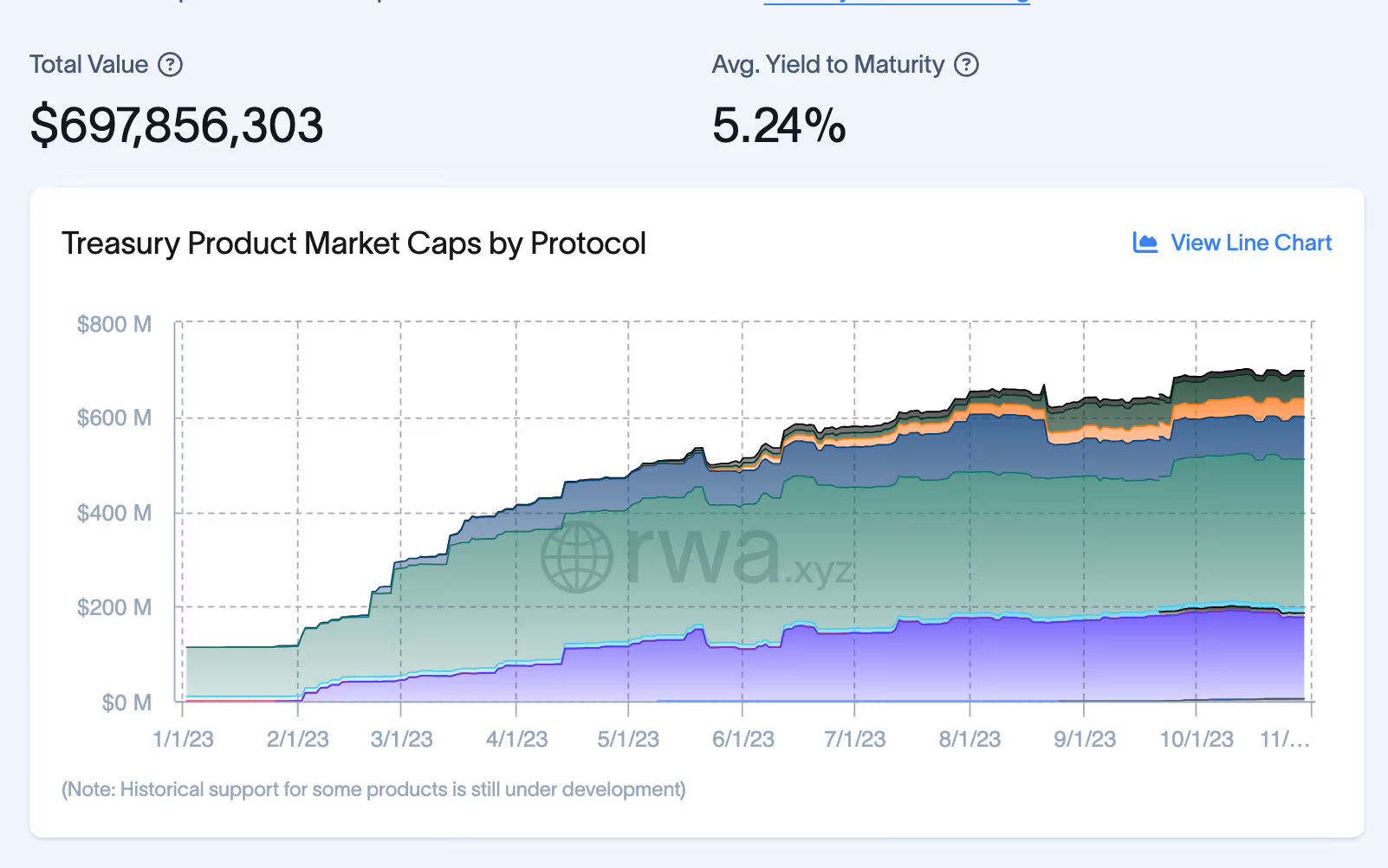

The market is growing rapidly. RWAs are projected to reach $30 billion in 2025, driven by institutional adoption and digital access to treasuries and credit. Imagine if a portion of your retirement portfolio could be moved, traded, or lent in seconds instead of days.

My first RWA wasn’t a bond, it was USDC, a digital stablecoin I used for a freelance payment. I didn’t think of it as “tokenized dollars” at the time, but it saved me weeks of settlement headaches. Have you ever considered that everyday assets, like property shares or corporate bonds, could be managed digitally, unlocking flexibility and yield previously reserved for big institutions?

RWAs in Action: Beyond the Hype

RWAs are not just a concept, they solve concrete inefficiencies in finance. Traditional securities often require two business days to settle, leaving buyers without ownership and sellers without funds. Digital representation of RWAs can reduce settlement to near-instant, cutting counterparty risk and transaction costs while improving liquidity.

For institutions, faster settlement frees up capital for reinvestment. For retail investors, it means immediate access to yields and tradable assets. Consider Siemens’ €60M digital bond, which settled in one day instead of two. Retail participants and treasurers alike can benefit from similar efficiency.

Real-World Examples:

BlackRock BUIDL Fund – allows access to digital Treasuries with institutional-grade efficiency.

Franklin Templeton On-Chain Money Market Fund – blends compliance with near-instant access.

Siemens’ Digital Bond – illustrates operational savings and faster liquidity.

Maple Finance and Ondo Finance – provide digital credit pools with automated settlement.

JPMorgan Onyx – shows institutional adoption of crypto for high-value settlements.

RWAs 101: Beginner to Pro

Real-World Assets come in different forms, and your entry point depends on your comfort level:

Beginner – Digital Cash & Treasuries

Think of this as your digital wallet. Stablecoins (like USDC) and tokenized Treasuries are simple, low-risk, and settle instantly. Perfect for freelancers, savers, or anyone who wants speed without complexity.

Intermediate – Bonds & Real Estate

Here you move from cash into assets that earn more. Tokenized corporate bonds and fractional real estate let you own a slice of something bigger. It’s like buying one room in a hotel instead of the entire building. Higher yields, but with more moving parts to learn.

Pro – Hybrid Pools & Advanced RWAs

This is the deep end. Hybrid credit pools, revenue-sharing agreements, and institutional-grade RWAs balance liquidity, yield, and compliance. They’re like hedge funds on-chain—highly rewarding but requiring careful risk management.

Once you understand the levels of RWAs, it’s easier to see what each real-world case study teaches us. Let’s look at some early movers—what worked, what didn’t, and what we can learn from them.

Lessons From the Frontlines

BlackRock BUIDL Fund – $300M raised in months.

Strength: Brand credibility + operational speed.

Challenge: Educating retail investors who still see RWAs as “too niche.”

Siemens Digital Bond – €60M issuance settled in one day

Strength: Reduced settlement risk + operational efficiency.

Challenge: Traditional buyers slower to embrace blockchain rails.

Maple: 10%+ yields through credit pools but exposed to borrower defaults.

Ondo: Lower but predictable returns via tokenized Treasuries.

Lesson: Different RWAs suit different appetites—risk-takers vs. conservative savers.

Beyond performance and risk appetite, what really makes RWAs valuable is their utility. Faster settlement, lower costs, and smoother user experience are what keep both institutions and retail investors interested.

Utility and User Experience: Why RWAs Work

RWAs don’t just make finance faster, they make it smoother.

Transaction Costs

Traditionally, securities trading involves brokers, clearinghouses, and custodians, each adding fees. RWAs cut these middlemen. A Siemens-style bond on blockchain may settle with 30–50% lower transaction costs.

User Experience

For institutions, near-instant settlement means billions in freed-up capital. For retail, it’s the difference between “waiting two days for your money” and “having it now.”

Imagine this: You sell a tokenized Treasury at noon and use the proceeds for a purchase that same afternoon. That’s finance working in internet time.

Of course, no financial innovation comes without trade-offs. RWAs unlock efficiency, but they also introduce risks—from liquidity gaps to regulation. Here’s how the industry is managing them.

Managing Risks

RWAs are powerful, but they’re not risk-free.

Liquidity Gaps

Challenge: Secondary markets are still young.

Mitigation: Buffered liquidity pools, automated market makers, and more exchanges listing RWAs.

Regulatory Uncertainty

Challenge: Different rules across regions.

Mitigation: Sandbox frameworks, compliance-first funds like Franklin Templeton, and alignment with EU’s MiCA guidelines.

Technical Failures

Challenge: Smart contract bugs, oracle errors, or custody issues.

Mitigation: Multi-sig custody, third-party smart contract audits, and redundant oracles.

The key lesson: risks aren’t eliminated, but layered safeguards make RWAs safer to use and more trustworthy than early DeFi experiments.

So where does that leave you as an individual investor? The best approach is to start small, build confidence, and gradually move up the RWA ladder. Here’s a simple action plan.

Beginner-to-Pro Action Plan

Start small with stablecoins. Example: Receive a freelance payment in USDC and notice the difference, minutes instead of weeks.

Move into digital treasuries. Instead of letting idle savings sit in your bank, park them in a tokenized Treasury fund and watch them accrue daily yield.

Try corporate bonds or real estate. Own a slice of a building or a fraction of a corporate bond—something that was once reserved for institutions.

Secure custody. Use a multi-sig wallet or platforms like JPMorgan Onyx to keep assets safe. Think of it as putting your car in a garage, not on the street.

Engage secondary markets. Sell a tokenized Treasury mid-quarter and instantly receive cash—something unthinkable in traditional bonds.

As you can see, RWAs aren’t just abstract concepts—they’re already shaping how money moves. The only question is whether you’ll watch from the sidelines or take part in the shift.

Conclusion: Step Into the Future

RWAs are quietly transforming finance. Faster settlement, broader access, and yield opportunities are real. Yes, challenges remain, liquidity, regulation, technology, but early movers stand to benefit most.

Stay curious. Test small. Join communities. In 2025, the real question isn’t whether RWAs matter, it’s whether you’ll claim your place in this new financial era.

RWAs are the quiet revolution of 2025. For early access to projects, strategies, and deep dives before they go mainstream, subscribe at canhav.com and be part of this shift from the ground up.