Beyond Payments: How to Put Stablecoins to Work for Yield, Treasury, and DeFi Ops

Unlock Instant Settlements, Cross-Border Savings, and Treasury Yield Strategies with Stablecoins in 2025: A practical guide for corporates, treasurers, and growth fintechs to use stablecoins.

My first crypto payment via USDC felt like wiring money without the bank delays. I watched a $4,200 invoice settle in ninety seconds, not three business days. The merchant on the other end, a freelance designer in Lagos, Nigeria, received the full amount minus a two-dollar gas fee. No correspondent banks. No weekend holds. Just pure velocity.

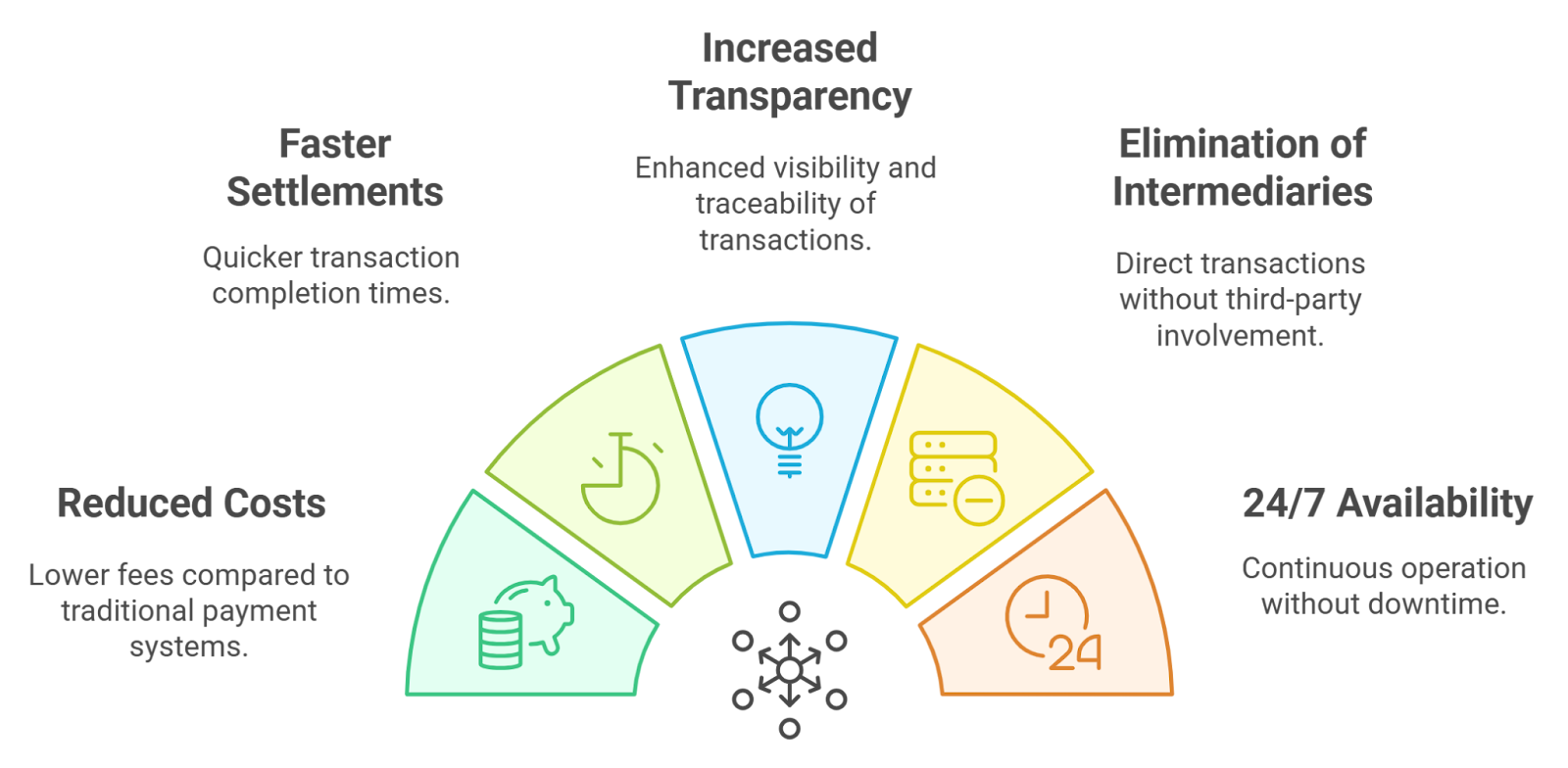

That moment clicked something for me. Stablecoins aren’t just crypto’s boring cousins anymore. They’re becoming the rails for how businesses move money, earn yield, and tap into decentralized finance without the Bitcoin rollercoaster. If you’re still thinking stablecoins are only for traders hedging volatility, you’re missing the bigger picture. These digital dollars are reshaping treasury operations, slashing cross-border fees by upwards of 90 percent, and opening doors to yield strategies that traditional finance can’t match.

Let’s dig into how stablecoins are moving beyond simple payments and becoming operational tools for businesses in 2025.

Can Stablecoins Really Cut Your Cross-Border Fees by 90 Percent?

Yes, and the math backs it up. Traditional wire transfers through banks typically cost between $25 and $50 per transaction, with correspondent banking fees adding another layer of expense. Factor in currency conversion spreads, and you’re looking at effective fees ranging from three to seven percent on international payments. That’s brutal for businesses running thin margins.

Stablecoin transactions on networks like Polygon or Solana cost pennies. According to Chainalysis, the median transaction fee for USDC on Polygon sits around $0.01, while Ethereum layer-2 solutions like Arbitrum average under $0.50. Even accounting for on-ramp and off-ramp fees through exchanges, total costs rarely exceed two percent. For a $10,000 international payment, that’s the difference between paying $500 in traditional banking fees versus $20 in crypto rails.

PayPal’s stablecoin, PYUSD, charges 0.99 percent for merchant transactions, enabling instant settlements. Compare that to Stripe’s 1.5 percent fee for USDC payments (still better than their standard 2.9 percent plus thirty cents for card processing), and the value proposition becomes clear. Merchants using stablecoin payment processors like Coinbase Commerce or Request Network report settlement times under five minutes, saving roughly $2 to $3 per $100 sale compared with PayPal and traditional processors with two to five business day standard, while eliminating 100 percent of chargeback liability.

Consider a small e-commerce merchant processing $250,000 a year in sales. By accepting USDC instead of traditional card payments, they could realistically save around $8,400 annually in processing fees. And since blockchain payments are irreversible, chargeback fraud disappears completely. That’s not just cost savings, that’s operational efficiency.

Industry data backs this up. According to Transfi’s merchant adoption report, U.S. merchants paid a total of $187 billion in card processing fees in 2024, a substantial chunk of which could be eliminated through stablecoin adoption. Settlement times under five minutes versus two to five business days for credit card processors represent a massive operational improvement.

Treasury Operations Meet Digital Dollars

Corporate treasurers are starting to see stablecoins as more than payment rails. They’re balance sheet assets that earn yield without touching traditional securities. Here’s where it gets interesting. Circle’s USDC Reserve Fund holds short-term U.S. Treasury bills and overnight repos, backing every USDC token one-to-one. That means holding USDC is effectively holding near-cash equivalents, but with programmability baked in.

Companies can now park operating capital in stablecoins and deploy it into DeFi protocols for yield. Platforms like Aave and Compound offer lending pools where USDC deposits earn four to six percent APY, significantly higher than the 0.5 percent offered by most corporate savings accounts. The catch? Smart contract risk and regulatory uncertainty. But for treasury teams willing to allocate a portion of reserves to these protocols, the risk-adjusted returns can outperform traditional cash management strategies.

MakerDAO’s DAI Savings Rate hit 8 percent in early 2024 before settling around five percent by year-end. Companies like Shopify have explored stablecoin integrations for cross-border vendor payments, signaling that mainstream adoption is accelerating.

Stripe announced in May 2025 that it’s making stablecoin-powered financial accounts accessible to businesses in 101 countries, a clear signal that enterprise adoption is moving fast. The idea isn’t to replace all cash holdings with crypto. It’s about diversifying treasury strategies and accessing yield opportunities that didn’t exist five years ago.

Think of it like this: stablecoins are the checking accounts, and DeFi protocols are the high-yield savings accounts. You wouldn’t keep all your money in a checking account earning nothing, right? Same principle applies here.

The DeFi Operations Playbook for Businesses

DeFi operations sound intimidating, but the core concepts are straightforward. Businesses can use stablecoins to access liquidity, earn passive income, and automate financial workflows without intermediaries. Here’s how some companies are doing it.

Liquidity pools on decentralized exchanges like Uniswap or Curve allow businesses to deposit stablecoin pairs, like USDC and DAI, to earn trading fees. Pool participants receive a percentage of every swap executed through the pool, typically ranging from 0.3 to one percent per transaction. According to DeFi Llama, total value locked in DeFi protocols surpassed $100 billion in early 2025, with stablecoin pairs representing over 40 percent of that volume.

Automated market makers handle the pricing, so there’s no need to actively manage positions. Businesses deposit assets, collect fees, and withdraw whenever needed. It’s passive income, but with smart contract risk. The key is starting small, testing the waters with one to five percent of liquid reserves before scaling up.

Another DeFi strategy gaining traction is flash loans. These uncollateralized loans allow businesses to borrow large amounts of stablecoins, execute arbitrage trades, and repay the loan within a single transaction block. Sounds complex, but developers are building user-friendly interfaces that automate the process. Companies with technical teams are using flash loans to optimize capital efficiency, moving funds between protocols to capture yield differentials without tying up capital long-term.

For businesses not ready to dive into DeFi directly, platforms like Maple Finance and Goldfinch offer structured credit products. Companies can lend stablecoins to institutional borrowers through these platforms, earning fixed yields between six and twelve percent depending on risk profiles. It’s closer to traditional lending but powered by blockchain infrastructure.

Merchant Adoption and Real-World Use Cases

Stablecoin adoption isn’t just theoretical. Merchants are integrating these payment options and seeing tangible benefits. Coinbase launched a platform in June 2025 designed to make stablecoins a go-to payment method for online transactions, bringing Shopify on board as a major integration partner.

A clothing retailer in Austin, Texas, posted on LinkedIn about switching to USDC payments for international suppliers. They cut payment processing times from seven days to under an hour and saved 5.3 percent on currency conversion fees. That’s real money hitting the bottom line.

Platforms like BitPay and Triple-A enable merchants to accept stablecoin payments and settle in fiat if they prefer. This hybrid approach reduces crypto exposure while capturing the speed and cost advantages. According to CoinGate’s 2024 Crypto Payment Report, stablecoins dominated merchant transactions in 2024, with TRON overtaking Bitcoin as the preferred network due to lower fees. Also, according to Chainalysis, merchant adoption of stablecoin payments grew 43 percent year-over-year in 2024, driven primarily by e-commerce and cross-border trade.

Stripe’s stablecoin rollout saw demand from 70 countries within months of launch. In the first 24 hours after enabling USDC payments in October 2024, Stripe saw significant merchant interest, signaling that businesses were ready for this payment option. The integration supports USDC on Ethereum, Solana, and Polygon networks.

Freelancers and gig workers are also jumping on the stablecoin train. Instead of waiting for PayPal or Wise to process international transfers, clients send USDC or USDT directly to wallets. Workers convert to local currency through peer-to-peer platforms or crypto ATMs, often at better rates than traditional remittance services. Paxful and LocalBitcoins report increased stablecoin volume, particularly in regions with limited banking infrastructure.

platforms used by businesses in 2024")

Many freelancers in markets like Manila report 8–12 percent higher take-home pay after asking clients to pay in USDC instead of bank transfers. The math is simple, clients skip high wire fees, and freelancers avoid local FX markups. Win-win.

Cast your vote and share your reasoning. The debate between stability and decentralization is ongoing, and your perspective matters. Also, give a reason for your response in the comments

Yield Strategies Without the Bitcoin Volatility

Bitcoin grabs headlines, but stablecoins deliver utility. For businesses focused on cash flow and predictable returns, stablecoins offer yield strategies without the stomach-churning price swings. Here’s where the opportunity lies.

Staking stablecoins on proof-of-stake networks isn’t the same as staking ETH or SOL, but liquidity staking derivatives are bridging the gap. Platforms like Lido and Rocket Pool allow users to stake assets and receive liquid tokens in return. While these platforms primarily focus on ETH staking, stablecoin integrations are emerging. Businesses can deposit stablecoins, receive tokenized receipts, and deploy those receipts into other DeFi protocols for compounding yields.

Yield aggregators like Yearn Finance automate this process. Deposit USDC, and the protocol routes funds to the highest-yielding strategies across multiple platforms. Returns fluctuate based on market conditions, but historical averages sit between four and eight percent APY. That beats most money market funds without requiring active management.

Real-world asset tokenization is another frontier. Platforms like Centrifuge and Backed Finance tokenize assets like invoices, real estate, and commodities, allowing businesses to collateralize these assets and borrow stablecoins. This unlocks liquidity without selling assets, creating flexible financing options that traditional banks can’t match.

According to Fireblocks’ 2025 Stablecoin Payments report, stablecoins accounted for nearly half of all transactions on their platform in 2024, representing 15 percent of global stablecoin volume. The report surveyed approximately 300 payment providers and banks globally, finding that speed, not just savings, is driving adoption.

For example, a logistics firm in Miami could use Centrifuge to tokenize outstanding invoices and borrow USDC against them — a process that typically delivers working capital in under 24 hours, compared to weeks with traditional factoring plus it would cost significantly more. Stablecoins enabled instant liquidity at a fraction of the cost.

Risk Management and Regulatory Considerations

Let’s talk about the elephant in the room: risk. Stablecoins aren’t risk-free, and businesses need to understand the trade-offs. Smart contract exploits, depegging events, and regulatory crackdowns are real concerns that can’t be ignored.

Tether’s USDT briefly lost its dollar peg in 2022, dropping to $0.95 during market panic. While it recovered, the episode highlighted counterparty risk. Not all stablecoins are created equal. USDC and PYUSD maintain transparent reserves and undergo regular attestations, while others operate with less oversight. Due diligence is non-negotiable.

Regulatory clarity is improving but remains fragmented. The European Union’s MiCA regulation sets standards for stablecoin issuers, requiring reserve transparency and capital requirements. The U.S. is still debating federal frameworks, leaving businesses to navigate state-by-state guidance. Companies operating internationally face a patchwork of compliance requirements, making legal counsel essential.

Smart contract audits are critical. Before depositing funds into DeFi protocols, verify that platforms have undergone third-party security reviews. CertiK and Trail of Bits are reputable auditors. Even with audits, exploits happen. Allocate only capital you can afford to lose, and never put operational funds at risk without proper insurance coverage.

Nexus Mutual and InsurAce offer DeFi insurance policies covering smart contract failures and depegging events. Premiums range from one to five percent of covered amounts annually, adding a layer of protection for businesses venturing into DeFi operations.

Future Trends Shaping Stablecoin Utility

What’s next for stablecoins? The roadmap includes deeper bank integrations, programmable payments, and central bank digital currencies competing for dominance. Banks like JPMorgan and Citi are launching proprietary stablecoins for institutional clients, blurring the line between traditional finance and crypto. These bank-issued tokens offer the speed of blockchain with the trust of established institutions.

Programmable payments are unlocking new use cases. Imagine payroll automatically disbursed in USDC every two weeks, with smart contracts handling tax withholdings and benefits contributions. Or subscription services that auto-deduct payments from stablecoin wallets without credit card processing fees. These aren’t futuristic concepts, they’re happening now on platforms like Superfluid and Sablier.

Central bank digital currencies are entering the chat. The Federal Reserve’s FedNow service launched in 2023, enabling instant bank transfers. While not a blockchain-based stablecoin, it signals that traditional finance recognizes the demand for faster settlement. CBDCs from China, the EU, and other nations will compete with private stablecoins, potentially fragmenting the market or driving innovation through competition.

Interoperability between blockchains is improving. Cross-chain bridges and protocols like LayerZero and Wormhole enable seamless stablecoin transfers across Ethereum, Solana, Avalanche, and other networks. Businesses won’t be locked into single ecosystems, allowing flexibility to optimize for speed, cost, and security based on specific needs.

According to Fireblocks’ 2025 Stablecoin Payments report, stablecoins accounted for nearly half of all transactions on their platform in 2024, representing 15 percent of global stablecoin volume. The report surveyed approximately 300 payment providers and banks globally, finding that speed, not just savings, is driving adoption.

Here’s a quick checklist for businesses exploring stablecoin operations:

Start with small allocations to test infrastructure and processes. Research stablecoin issuers and verify reserve transparency before committing funds.

Evaluate payment processors that support stablecoin settlements. Consult legal advisors on compliance requirements in your jurisdiction.

Audit DeFi protocols before depositing capital. Consider insurance coverage for smart contract risks.

Monitor regulatory developments that could impact operations.

Train finance teams on wallet security and custody best practices.

What This Means for Your Business

Stablecoins aren’t replacing dollars or euros anytime soon, but they’re carving out a permanent place in the financial ecosystem. Businesses that understand how to leverage these tools gain competitive advantages: faster payments, lower costs, and access to yield strategies unavailable through traditional banking. This table below highlights key differences between DeFi vs Traditional Finance. Now do the maths.

and traditional finance across multiple aspects, including accessibility, transaction speed, intermediaries, costs, transparency, regulation, customization, risk, yield potential, and user control.")

The learning curve is real. Wallets, gas fees, smart contracts, these concepts take time to master. But the payoff justifies the effort. Companies moving early are building operational efficiencies that compound over time, much like early internet adopters who embraced e-commerce in the late nineties.

If you’re on the fence, start experimenting. Open a Coinbase account, buy $100 of USDC, and send it to a friend. Experience the speed firsthand. Explore payment processors that integrate stablecoins. Talk to your treasury team about yield strategies. The technology is mature enough for production use, and the ecosystem continues improving month by month.

Share your payment wins below. Have you integrated stablecoins into your business? What challenges did you face, and what benefits did you unlock? The community learns from real-world experiences, and your story could help another business make the leap.

Subscribe to Canhav for crypto trends, stablecoin strategies, and merchant guides. Get alerts on 2026 updates!

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or investment advice. Stablecoins and DeFi protocols carry risks including smart contract vulnerabilities, regulatory changes, and market volatility. Always conduct your own research (DYOR) and consult qualified professionals before making financial decisions.