Stablecoins are cryptocurrencies pegged to assets like the US dollar, commodities, and other crypto assets, or they are artificially controlled through algorithms.

The stablecoin sector is the fastest-growing bridge between traditional finance and blockchain. According to Citi’s Digital Dollars Report, their market cap recently crossed $230 billion and could grow to $2 trillion by 2028. These “digital dollars” are increasingly used as “cash on-chain,” enabling faster, cheaper cross-border payments and innovative financial services. In fact, in a few months, roughly two-thirds of crypto transactions are estimated to involve a dollar-denominated stablecoin.

Stablecoins are the most critical use case of blockchain and cryptocurrencies for enterprises!

When I first conceived this Stablecoin Market Map during my Master’s in Financial Innovation & Technology at Queen’s University (Smith School of Business), the idea was to organize the ecosystem into layers. It reflects my journey and way of thinking. However, there are other market maps like the one by Artemis, which I also highly recommend looking into as you explore the market. The map created by me, is inspired by Systems Design, which I believe is the best way of understanding each ecosystem piece and how projects (including ours) fit together. I have been creating market maps and systems design to understand markets for years, including a popular Metaverse Market Map, which I created to understand the intersection of web3 and mixed reality in 2022.

This article represents a layered view of the stablecoin world. Each layer is crucial, from the blockchains that settle tokens through the applications (payments, remittances, etc.), to the media, regulators, and investors monitoring the space. I’ve enriched the map with many examples of projects and companies (with links) so you can dive deeper into each.

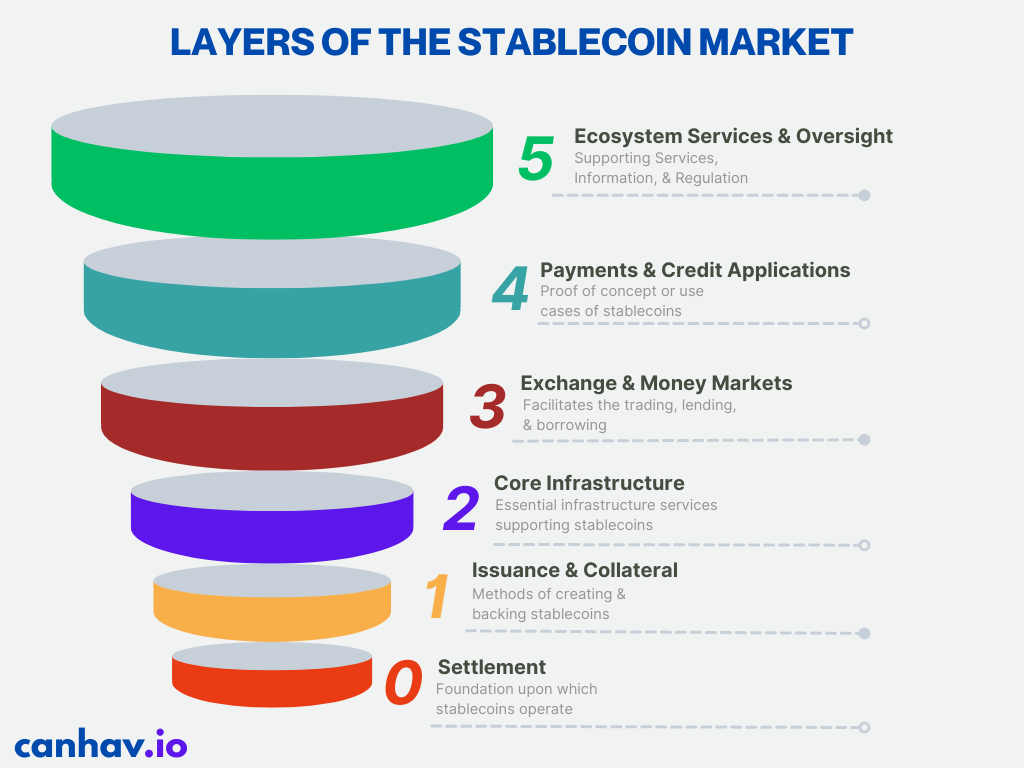

Layer 0: Settlement Layer: Chains, L2s, and Bridges

At the foundation is the Settlement Layer — the blockchains and networks that host stablecoins and the bridges that move them between chains. This layer shapes the speed, cost, and reach of stablecoins.

0-1. Blockchains & L2s

Stablecoins live on many chains. Here are some of the most prominent players in the market:

Ethereum is home to the largest stablecoins thanks to its security. However, without the right L2, gas fees can be high.

Solana offers speedy, low-fee transactions and is increasingly popular for stablecoin use.

Tron hosts a considerable share of USDT volume (especially in Asia).

Emerging layer-2 networks like Arbitrum and Optimism bring Ethereum security with much lower fees. Uniswap’s major stablecoin markets are active on Arbitrum, for example. Other chains like Binance Smart Chain and Avalanche also run fiat-backed tokens.

In short, major stablecoins now exist on dozens of chains to balance accessibility with cost.

0-2. Bridges & Interoperability

Because users and apps span many chains, bridges let stablecoins move between them.

1. Circle’s CCTP is a native protocol that sends USDC across chains by burning/minting, now upgraded (CCTP V2) to cut settlement time from ~15 minutes to seconds.

2. Cross-chain protocols like Wormhole and LayerZero connect many ecosystems. LayerZero, for instance, links over 100 blockchains (Ethereum, Solana, Tron, etc.) in a unified network. These bridges are improving rapidly; the newest designs reduce latency and bolster security, enabling use cases like instant global transfers.

Stablecoins’ multi-chain presence ensures they can reach any user or market. This diversity also demands careful design: each blockchain has trade-offs in security, speed, and decentralization. Bridges must be trusted or decentralized; many now use cryptographic proofs or decentralized relayers to move tokens securely. The net effect is that your stablecoin (say, USDC) can hop from Ethereum to Solana to Bitcoin’s Lightning Network, making it “cash on-chain” that’s accessible anywhere!

Layer 1: Issuance & Collateral

Layer 1 covers how stablecoins are created and backed — the various models that keep them “stable”. I have categorized them into four types:

1-A. Fiat-Backed Issuers

Fiat-backed stablecoins hold real-world currency or equivalents in reserve at a 1:1 ratio. Examples include:

· Tether (USDT): The largest stablecoin by market cap (~$150B as of 2025). Tether claims full backing by cash and equivalents, and regularly publishes attestations. It runs on Ethereum, Tron, and other chains.

· Circle (USDC): The second-largest, backed by US dollars and U.S. Treasurys. USDC emphasizes transparency and compliance as Circle provides monthly audits. Notably, USDC’s reserves mostly sit in short-term Treasuries, so its growth has boosted Treasury demand!

· PayPal USD (PYUSD): Launched in 2023, issued by Paxos, with deposits and Treasuries backing it. Targeted at PayPal’s vast user base for seamless crypto-USD transactions.

· Binance USD (BUSD): Issued by Paxos (until late 2023), fully backed by USD, and backed by strict NYDFS regulation until it wound down.

· TrueUSD (TUSD): Another fiat-backed token with regular attestations.

These fiat models are straightforward: 1 USDT or 1 USDC = 1 USD of reserves. Due to a rapidly growing interest in these fiat models and enterprise adoption, new rules (like the EU’s MiCA) now require 100% backing, independent audits, and redemption guarantees. The trend is toward greater transparency. For example, Circle’s provable-reserves tool lets anyone verify USDC’s USD backing in real time.

1-B. Commodity-Backed Issuers

These stablecoins are backed by physical assets, usually precious metals:

· Pax Gold (PAXG): Each token represents one troy ounce of gold stored in vaults (Brink’s, etc). PAXG blends blockchain efficiency with actual gold ownership. Holders can redeem tokens for physical gold (minus fees, of course).

· Tether Gold (XAU₮): Similar to PAXG, each XAU₮ token corresponds to one ounce of London Good Delivery gold. It’s basically a blockchain-wrapped gold holding, making it easier to trade and store gold.

· Perth Mint Gold Token (PMGT): Issued by Australia’s Perth Mint, fully backed by gold reserves with a government guarantee.

· Digix Gold (DGX): Another on-chain gold-backed token, each DGX = 1 gram of LBMA-standard gold.

Commodity tokens allow fractional and programmable ownership of gold or other tangible assets. They appeal to those who want an inflation hedge (like gold) but with crypto speed!

By storing physical assets off-chain in custodial vaults, these tokens depend on transparency (proof of reserve) and audit mechanisms to assure holders of the backing. As with fiat stablecoins, innovations like on-chain oracles (see Layer 2) can verify these reserves publicly.

1-C. Crypto-Collateralized Protocols

Crypto-backed stablecoins are over-collateralized by other cryptocurrencies via smart contracts:

· MakerDAO’s DAI: The longest-running DeFi stablecoin. Users lock ETH or other crypto in Maker Vaults (formerly Collateralized Debt Positions) to mint DAI. The system requires excess collateral (e.g. >150%) to absorb volatility. Governance (i.e., MKR holders) sets stability fees (interest rates) and collateral types. DAI is decentralized (no single issuer, unlike Circle’s USDC), and its collateral vaults hold thousands of ETH, WBTC, etc.

· Aave GHO: A newer stablecoin from Aave’s lending protocol. Users can mint GHO by depositing collateral (like USDC) and paying interest to the Aave DAO treasury. This expands on Aave’s model, making stablecoins a first-class asset for DeFi lending.

· Liquity LUSD: An algorithmic loan scheme where users deposit ETH to borrow LUSD at a minimum 110% collateral ratio. Liquity charges a one-time fee, but no interest, and relies on liquidations to maintain the peg. (LUSD often trades close to $1 if ETH is stable.)

· Neutrino USD (USDN): Backed by WAVES tokens; a bit more niche.

Crypto-collateral designs avoid trust in central institutions using on-chain collateral and liquidation mechanics. They tend to be highly over-collateralized to guard against market swings. These protocols require careful risk models (e.g. what happens if ETH drops 50% quickly?). After the failure of TerraUSD in 2022, the DeFi community has favored heavily collateralized hybrids (like Frax, see 1-D) over pure algorithmic schemes. Still, crypto-collateralized stablecoins are key to fully decentralized financial stacks, as they can be minted and traded without any fiat gateway!

1-D. Algorithmic / Hybrid Issuers

Algorithmic stablecoins aim to maintain a peg through on-chain algorithms, often with some collateral:

· Frax (FRAX): The leading fractional-algorithmic model. FRAX is backed partly by collateral (USDC or other stablecoins) and partly stabilized by minting/burning of its share token FXS. The protocol adjusts the collateral ratio to target $1 value. For example, if FRAX > $1, it might mint FRAX and sell for collateral to bring the price down, and vice versa.

· TerraUSD (UST) (RIP): Terra’s UST (now Terra Classic USTC) was a famous algorithmic stablecoin that collapsed in 2022, triggering a massive market crash. It aimed to stay at $1 through mint/burn with the LUNA token, but lost its peg due to a bank run dynamic. This was one of the biggest crypto stories in 2022, which led to a ripple effect, leading to many other crypto firms being exposed!

· Tron USD (USDD): A Tron-native stablecoin that uses a partial collateral and incentive model. It is pegged to USD and backed by a mix of USDT, TRX, and other assets held by the Tron DAO Reserve.

· Reflexer’s RAI: Not pegged to fiat, but an algorithmic stable-like asset that targets one-to-one against a moving “redemption price.” RAI is backed by ETH and stabilized algorithmically; it’s an experiment in non-pegged stability.

· DEI (formerly FEI): A protocol launched in 2021 to experiment with direct peg maintenance and bonding curves, though it faced challenges in fully maintaining the peg.

After Terra’s crash, the market shifted away from pure algorithmic designs. Hybrid models (like Frax, USDD) with actual collateral or protocol reserves and code-driven mechanisms became favoured. Some propose multi-collateral algorithmic systems (adding crypto, fiat reserves, and on-chain revenue sources) to enhance resilience.

Studying and observing the four types of stablecoins, I realized that while each of them has benefits, they all have major flaws as well and have been routinely exposed. This is exactly what has led me to work on multi-currency stablecoins like the CXDR stablecoin. The coin is pegged to a basket of major currencies, using IMF SDR weights. By combining different currencies with strategic weights which are over-collateralized, CXDR aims to be a robust global liquidity asset for trade!

The bottom line: Stablecoins come in many flavours in issuance and collateral. Fiat-backed coins dominate market share today because of simplicity and regulatory clarity. Commodity tokens offer a bridge to traditional stores of value. Crypto-collateralized and algorithmic coins power decentralized finance but require careful design. My (biased) prediction is that the future will likely see more hybrids, including multi-currency, over-collateralized models like CXDR, that blend the best of all types for stability and utility.

Layer 2: Infrastructure & Plumbing

Layer 2 is the infrastructure that powers stablecoin operations behind the scenes. It includes custody services, oracle networks, compliance tools, and gateways that move between fiat and crypto.

2–1. Custody & Trust Companies

These are regulated entities that hold the actual reserves backing fiat and commodity tokens. For example:

Paxos Trust Company is the custodian for Pax Gold and was the issuer of BUSD; it provides audited reserves and regulatory filings.

Anchorage Digital is a federally chartered crypto bank offering institutional custody for cryptocurrencies and tokenized assets.

Other major players include Fireblocks and Coinbase Custody, which provide secure vaults for crypto collateral and sometimes fiat reserves. As regulators tighten oversight, these custodians increasingly obtain banking charters and subject themselves to trust laws, ensuring that stablecoin reserves are fully audited and segregated.

2–2. Proof-of-Reserve & Oracle Networks

DeFi protocols and stablecoin issuers rely on oracles to fetch external data. Now, Proof-of-Reserve oracles specifically verify that on-chain assets match off-chain holdings. For example:

Chainlink Proof-of-Reserve monitors issuers' blockchain addresses and checks them against attested reserves.

Pyth Network provides real-time price feeds for various assets, ensuring stablecoins maintain pegs (especially crypto-collateralized ones).

Other oracle networks like Band Protocol and Provable can also bring real-world data on-chain.

As stablecoin users demand transparency, these oracles offer automated assurance that, say, 1 USDC is truly backed by $1 of T-bills, which results in building trust without relying solely on siloed audits.

2–3. Stablecoin-as-a-Service & APIs

Some companies offer turn-key infrastructure to create and manage stablecoins.

Stably provides a white-label stablecoin issuance platform: businesses can mint their own dollar tokens using Stably’s regulated reserves.

Orchestra Labs has developed a blockchain (“Symphony Chain”) and compliance toolkit specifically for stablecoins.

CBDC platform by Ripple is used by many central banks and institutions to evaluate for digital currency issuance (though more for central bank tokens than private stablecoins, the tech overlaps).

These APIs and services allow non-crypto companies to launch tokens. For example, a gaming company could issue an in-game stablecoin redeemable for USD, leveraging existing stablecoin rails. As regulations expand, these platforms increasingly include automated KYC/AML and audit features.

2–4. On/Off-Ramps (Fiat Gateways)

For stablecoins to matter, users need easy ways to move between bank accounts and crypto wallets. Services like MoonPay and Transak plug into wallets and apps to enable credit-card or bank transfers into stablecoins. Kado focuses on ultra-low-fee, fast on-ramps specifically for stablecoins. Others include Banxa, Rocket Money, and Ramp Network.

These gateways are streamlining: instant ACH, multiple currency support, and compliance checks are becoming standard. For businesses, APIs from fintechs like Circle allow direct fiat-USD deposits that mint USDC on-chain, bridging with minimal friction.

2–5. Liquidity Providers & Market-Makers

A subtle but crucial piece is the firms that keep stablecoin prices tight and liquid. Wintermute is one of the largest crypto market makers, providing deep liquidity for stablecoin trades across CEXs and DEXs. Cumberland (DRW) and Jump Trading similarly commit capital to stabilize stablecoin prices.

They use sophisticated algorithms to arbitrage any tiny price differences between exchanges, which is vital since stablecoins trade across hundreds of markets. As the ecosystem grows, these liquidity firms invest in cross-chain market-making: for example, if USDC is slightly under $1 on one chain, they’ll buy it and move it via a bridge to sell it where it’s slightly above $1, keeping the peg intact globally.

This infrastructure layer is like plumbing. This means they are mostly invisible to end users, but the stablecoin “water” wouldn’t flow without it. Advances here include faster oracles, better custody audits, seamless bank integrations, which have given confidence to everyone from crypto traders to corporate treasurers that stablecoins are reliable, liquid, and ready for real-world finance.

Personally, improvements in seamless bank integrations and custody audits are critical if multi-currency stablecoins like CXDR are to become a reality, as enterprise users, especially those trading internationally, need to ensure that the medium used to enable trade is reliable and mitigates more risks than it creates!

Layer 3: Markets and Money-Market Protocols

Layer 3 covers the trading and yield services for stablecoins. Once you have stablecoins, how do you exchange, lend, or leverage them? This layer includes exchanges, lending protocols, and derivatives markets.

3–1. Centralized Exchanges & Brokerages

The most prominent venues for stablecoin trading are CEXs.

Binance handles a massive volume of USDT, USDC, BUSD, etc., across a lot of trading pairs. Coinbase is a regulated American exchange offering fiat pairs with USDC, and it actively integrates new stablecoins (e.g. USDP). Kraken and Bitstamp similarly allow traders to swap stablecoins with fiat or crypto. These exchanges often list multiple stablecoins side-by-side, letting users pick by trust or region (for instance, EU residents might prefer USDC for MiCA compliance reasons). As regulations tighten, exchanges play by rules: for example, Kraken requires identity verification for fiat on/off ramps. Despite crypto’s DeFi ethos, CEXs remain important for stablecoin liquidity and onboarding many users from fiat.

3–2.Decentralized Exchanges (AMMs)

On-chain trading of stablecoins happens via Automated Market Makers. Uniswap is the largest DEX by volume, with many stablecoin pools (USDC/ETH, USDC/USDT, etc.) on Ethereum.

Curve Finance specializes in stable-to-stable swaps (like USDC<->DAI or USDT<->USDC) with extremely low slippage — its curve-shaped liquidity pools use a special formula to keep stablecoin prices equal.

Other notable DEXs include Balancer, SushiSwap and PancakeSwap.

These decentralized venues allow anyone to swap stablecoins without an account, and liquidity providers earn fees. Innovations like concentrated liquidity (Uniswap v3) and new pool algorithms continuously improve capital efficiency and minimize impermanent loss.

On L2 and cross-chain DEXs (e.g. Polygon, Arbitrum), new players like Aerodrome and Synapse are optimizing for even cheaper stablecoin swaps.

3–3. Yield / Money-Market Protocols

People often lend out stablecoins for interest or use them as collateral. Leading platforms include Aave and Compound.

On Aave, for instance, you can deposit USDC or DAI into a liquidity pool and earn interest (from borrowers). Compound works similarly. These protocols “tokenize” your deposit into interest-bearing tokens (e.g., aUSDC, cUSDC) that track yield.

There are also specialized yield projects: Ondo USDY is a “stablecoin fund” that holds tokenized U.S. Treasuries and pays yield in USDY (an ERC-20 stable token).

Yearn Finance automates moving stablecoins between the best interest sources. More recently, platforms are tokenizing real-world assets as collateral to earn yield: for example, mStable or Centrifuge link stablecoins to loans or invoices.

The trend is blending DeFi lending with regulated assets: stablecoin money markets may hold short-term government bonds, Repo agreements, or corporate paper to get a risk-managed yield. This makes them less correlated with crypto price swings. For example, Aave recently integrated real-world yield markets (like tokenized funds) so you can lend stablecoins against traditional credit.

3–4. Perpetuals & Derivatives Markets

Stablecoins are also used as collateral and settlement currency in crypto derivatives. Decentralized perpetual exchanges like dYdX let users trade perpetual futures (i.e., leveraged bets) on coins, with USDC or DYDX tokens as collateral.

GMX on Arbitrum provides on-chain perpetuals with zero slippage and chain-agnostic collateral (including many stablecoins).

On the CeFi side, Binance Futures and Bybit offer large perpetual and futures markets where positions are margined and settled in stablecoins. These derivatives venues add depth to the market: if a stablecoin deviates from $1, arbitrageurs can short or long it with leverage until it snaps back. As with spot markets, derivatives for stablecoins are evolving: risk management systems (like auto-liquidation triggers) are continuously improved to prevent liquidity crises.

Layer 3 thus turns stablecoins from idle tokens into active financial instruments. They become money-market instruments (loaned for yield), trading instruments (swapped on CEX/DEX), and collateral for sophisticated strategies. Through these markets, stablecoins maintain liquidity and keep pegs, while earning returns and powering new financial primitives.

I believe the CXDR token and multicurrency pegs can help users engage in these markets internationally without relying on a single nation or currency. This allows more practitioners internationally to trade in the markets on a level playing field!

Layer 4: Applications

Layer 4 is where stablecoins meet real-world use cases: actual payment, credit, and business applications that leverage stablecoins. This layer, which is probably of most interest to the readers of this article, includes everything from retail point-of-sale to enterprise treasury.

4–1. Consumer Payments & POS

Stablecoins can power everyday payments.

Flexa is a network that lets merchants accept crypto payments, which are instantly converted to local currency or stablecoins.

BitPay processes crypto payments for vendors, including stablecoin options.

Some online platforms like Shopify allow merchants to enable cryptocurrency payments, which often route through stablecoins for pricing. For instance, a Shopify store might accept USDC via a payment plugin, giving the merchant immediate USD (off-chain or on-chain).

Adoption is growing: stablecoins offer faster settlement and lower fees than credit cards. As a result, payment apps and point-of-sale systems are adding stablecoin support. Over time, I expect more shops and e-commerce sites to offer a “Pay with USD Coin” button alongside Visa or PayPal, especially in regions with volatile local currencies.

4–2. Crypto Debit Cards

Several platforms issue crypto debit cards that let users spend crypto (including stablecoins) anywhere Visa/Mastercard is accepted.

Coinbase Card and Crypto.com Card automatically convert your crypto to fiat at checkout; many users hold stablecoins on the backend for convenience.

A recent trend is cards that directly settle in stablecoins: for example, a prototype from Mastercard and Circle (see Payment Network Integrations) could let Crypto.com Card spend USDC directly.

These cards bring crypto into daily life with rewards (cashback in crypto) while ultimately using stablecoins as the underlying funds.

4–3. Payment-Network Integrations

Traditional rails are integrating stablecoins too.

In 2020, Visa became the first major payments network to settle a transaction in USDC on-chain. Visa has since piloted USDC settlement with Crypto.com and Anchorage, enabling merchants to receive funds in stablecoins instead of USD.

Mastercard announced this year that it will allow merchants to settle in stablecoins (like USDC, USDP) through partners like Paxos and Circle.

These partnerships mean stablecoins can flow into existing payment infrastructure. For example, a remittance service might send a payment in USDC, which arrives at the receiving bank via Visa’s network. These efforts mark an important convergence: major card networks are finally treating stablecoins as a new class of settlement currency.

4–4. Remittance Apps

Stablecoins shine for cross-border personal transfers.

MoneyGram & Stellar: As a key example, MoneyGram partnered with the Stellar network to settle remittances in USDC. Wallets on Stellar can convert USDC to local cash instantly via MoneyGram’s extensive agent network, cutting remittance times to minutes.

Afriex in Africa lets users send USD, GBP, EUR as stablecoins (on Stellar or other chains) to recipients who cash out in local currencies.

Lemon Cash in Latin America uses stablecoins to move money across Argentina and neighboring countries.

These fintech apps harness stablecoins’ low-cost rails to bypass slow banking channels, slashing fees. The IMF notes that blockchain “can increase speed and reduce costs for cross-border remittances”. This IMF stance on stablecoins is an insight as their SDR continues to stand the test of time with changes that reflect macroeconomic conditions.

4–5. Cross-Border FX & Trade Payments

Beyond person-to-person, stablecoins facilitate institutional cross-border transactions.

Ripple’s ODL (On-Demand Liquidity) uses XRP as a bridge asset, but also works with stablecoins like USDC.

JP Morgan’s Onyx Platform (JPM Coin)is a permissioned bank-based stablecoin for B2B USD transfers between institutional clients.

Rail, still an emerging platform, uses stablecoins for instant international transfers, claiming settlement in hours instead of days.

Companies are exploring stablecoins as a complement to SWIFT/GPI: for instance, remittance corridor projects between Asia and Africa often propose USD stablecoins to offset local currency weakness.

My project CXDR by canhav.io envisions a stablecoin pegged to a basket of IMF currencies (like SDR) to settle international trade invoices. By pooling multiple major currencies, CXDR could reduce currency risk for exporters, offering an “ultra-stable” payment rail across borders!

4–6. P2P and Wallet Transfers

Many consumer wallets make it easy to send stablecoins to anyone, anytime. Integration with payment apps and protocols means users can “Pay anyone with USDC” via QR code or username.

Valora Wallet on Celo allows instant peer-to-peer stablecoin transfers on mobile.

Bitcoin’s Lightning Network is also being adapted for stablecoins: projects like Lightning Labs have proposed pegging tokens (like USDT) on Lightning channels for instant value transfer.

The trend is user-friendly wallets where crypto novices won’t even notice they are using blockchain; behind the scenes, it’s just USD moving on a chain. As the IMF notes, stablecoins let people “remain in the crypto universe without having to cash out into fiat”, effectively making crypto easier for everyday transactions.

4–7. B2B Payments & Invoicing

Businesses are building payment rails with stablecoins.

Circle’s Treasury & Payments API allows companies to hold, send, and receive USDC as part of their software. For example, a SaaS company could pay contractors in USDC instantly worldwide.

Request Finance is an invoicing tool that lets freelancers bill in USD but be paid in stablecoins; it simplifies crypto accounting for businesses. On the enterprise side, blockchain-based supply chain networks are exploring stablecoin-based invoicing to shorten payment cycles.

4–8. Treasury & Cash Management

Organizations adopting crypto need secure treasury tools.

Fireblocks offers an enterprise platform to securely store and transfer digital assets (including stablecoins) with multi-party computation keys and compliance checks.

Gnosis Safe Treasury provides a multisig wallet system that corporations and DAOs use to hold stablecoins and execute multi-sig payments.

These platforms integrate with DeFi too: companies can pool idle stablecoin cash in yield-generating protocols for extra returns, all while maintaining high security. The key advancement here is giving treasurers the comfort (via audits, insurance, multi-sig controls) to treat stablecoins like any other currency in the corporate treasury.

4–9. Micro-Loans & Credit

Finally, stablecoins enable new credit products, especially in underserved regions.

Goldfinch Protocol uses stablecoins to lend to small businesses in emerging markets without collateral, underwriting loans on-chain and paying out in stablecoins.

Union Credit and similar DeFi credit protocols allow undercollateralized loans, letting trusted users borrow stablecoins with minimal crypto collateral.

The ability to borrow, lend, and pay interest in stablecoins is bringing credit to people who can’t access traditional loans. These systems are evolving to incorporate real-world credit scores and identity KYC, bridging DeFi lending with conventional finance.

Layer 4 demonstrates real uses: from buying coffee to paying an overseas supplier in USDC. It’s where stablecoins answer the question “So what?” — providing tangible solutions. The examples above cover retail, corporate, and government use cases.

One common thread: stablecoins offer speed and programmability (blockchain automation) that legacy systems lack.

In developing economies, they could transform remittances and savings, while in developed markets, they open new products (like programmable money with conditional settlement). However, stablecoins must diversify beyond a 1:1 peg with the USD for developing economies and mass adoption. There is a finite amount of USD in the market, which is controlled by one government. The spirit of blockchain and crypto should move the sector towards diversification, with USD being a major player, of course!

Layer 5: Oversight & Ecosystem

The final Layer 5 encompasses the oversight, analytics, and community ecosystem around stablecoins. It’s the support structure: compliance firms, regulators, media, and investors that keep the system running smoothly.

5–1. Compliance / AML Monitoring

Stablecoins must satisfy anti-money-laundering (AML) laws.

Firms like Chainalysis and TRM Labs provide on-chain analytics and monitoring for blockchain activity. They help exchanges and institutions flag suspicious stablecoin transactions.

For example, if a blacklisted wallet tries to cash out Tether, the AML software spots it. As regulators (e.g. FinCEN in the US) impose more rules, these monitoring tools are critical. Increasingly, stablecoin issuers themselves integrate these services, ensuring compliance at the protocol level (e.g. KYC-gated minting, whitelists for large transfers).

5–2. Insurance & Risk Coverage

Blockchain is new territory, and stablecoins carry risks (smart contract bugs, reserve failures, de-pegs).

Nexus Mutual offers DeFi smart-contract insurance; users can insure their stablecoin positions against contract exploits.

New products like Chainproof specialize in stablecoin de-peg insurance. They pay out if a stablecoin loses its peg due to issuer negligence or technical failure.

In a maturing market, we expect an entire suite of crypto insurance products (custody insurance, protocol failure insurance) to underwrite stablecoin risk, much like banks buy FDIC for fiat.

5–3 Ratings & Assessors

Independent analysts evaluate stablecoin quality. For example, S&P Global has published stablecoin ratings (an “S&P Stablecoin Report”) assessing issuers’ reserve practices and governance. Niche firms like Particula Analytics focus on deep dives into stablecoin reserve transparency and peg stability. These evaluators create models that combine traditional finance metrics (liquidity ratios, audit frequency) with on-chain data (transaction volume, decentralization). As the sector grows, we’ll likely see more third-party ratings (akin to credit ratings) for stablecoins, helping institutional investors distinguish a “gold-standard” stablecoin from a risky one.

5–4. Analytics & Data Platforms

On-chain data providers give insight into stablecoin flows.

Nansen tracks wallets and token movements; one can see how many wallets hold USDT or how much stablecoin is in DeFi TVL.

Glassnode publishes metrics like stablecoin supply, velocity, and net issuance.

Dune Analytics is a community platform where anyone can build dashboards. There are many community dashboards analyzing stablecoin market share or flows between chains.

These tools help researchers and traders understand market trends (e.g. a sudden surge in Tether inflows could signal more buying pressure on crypto assets, as one on-chain analyst noted). As stablecoins enter traditional finance, new data vendors may emerge to offer real-time compliance and risk scores.

5–5. Media & Research

Crypto news outlets and research firms follow stablecoins closely. CoinDesk and The Block report on regulatory developments and market moves (like our Citations from both).

Messari provides in-depth research reports and data on stablecoin protocols. There are specialized newsletters and blogs dedicated to stablecoins (for instance, Celo and Stellar communities have active blogs on stablecoin use). This information flow educates both industry insiders and curious public about what’s happening. It also creates accountability: e.g. investigative stories on where stablecoin reserves really are can lead to audits or reforms.

5–6. VCs & Institutional Investors

Venture firms are funding next-gen stablecoin infrastructure.

Pantera Capital and Andreessen Horowitz (a16z) have backed multiple stablecoin and DeFi projects. Castle Island Ventures focuses explicitly on crypto and stablecoin infrastructure.

These investors provide capital and expertise in banking and regulation (e.g., Castle Island includes former Fed staff).

On the institutional side, we see banks and fintechs starting stablecoin funds or integrating them into offerings. For example, digital-asset funds (like the upcoming BlackRock BUIDL series) may include exposure to stablecoin yields or reserves.

Even Money Market Funds (MMFs) are exploring tokenization: e.g. a tokenized MMF might let clients hold a digital share that represents a basket of T-bills and commercial paper, akin to a crypto money-market stablecoin.

5–7. Investment Wrappers / Funds

Traditional finance is dipping its toes into stablecoins indirectly. BlackRock and WisdomTree have launched crypto funds (some include stablecoin exposure) that trade on stock exchanges. The idea of “tokenized money market funds” has emerged: these are fund shares on a blockchain, providing something like an on-chain stablecoin but backed by real-world securities. In some ways, these blur the lines between stablecoins and e-money. The key trend is institutionalization: stablecoins will not remain purely retail tools, but will be integrated into asset management products.

5–8. Regulators & Policymakers

Finally, no ecosystem layer is complete without oversight. Major regulators around the world are crafting stablecoin rules.

In the U.S., bodies like the Federal Reserve, the President’s Working Group on Financial Markets, and Congress are actively debating legislation for stablecoin governance. The NYDFS imposes New York trust regulations on issuers like Paxos and Circle.

In late 2024, the EU’s MiCA framework came into force, requiring 100% reserves and audits for stablecoins in Europe.

Other jurisdictions have varied approaches: Singapore and Hong Kong are positioning themselves as crypto hubs with clear rules, whereas some countries (like China) are banning private stablecoins outright.

The S&P Global analysis has stated that MiCA’s strict rules and emerging U.S. legislation will likely drive global stablecoin adoption by giving trust to larger users.

Regulators are also coordinating on issues like capital controls: stablecoins can cross borders easily, which worries some authorities about “circumvention” of regulations on money movement. So, we see committees and working groups (e.g. the Financial Stability Board) focusing on global standards.

In summary, Layer 5 covers the ecosystem that surrounds stablecoins: the firms that watch the networks, the media that reports, the VCs that fund, and the regulators that rule. The evolving oversight and ecosystem are ensuring those risks are managed. For example, USDC’s reserve in Treasuries has actually fed back into mainstream finance by modestly increasing demand for T-bills.

Ultimately, how stablecoins integrate with the existing financial infrastructure (or remain a parallel system) will depend on this ecosystem’s development.

Conclusion: Navigating the Stablecoin Map

This layered “Stablecoin Market Map” outlines the complexity of the stablecoin world. From the chains and bridges (Layer 0/Settlement) to the issuing models (Layer 1), through the plumbing infrastructure (Layer 2) and the trading/yield markets (Layer 3), into the concrete applications (Layer 4), all the way to the oversight and support (Layer 5) — every layer is interdependent. I’ve worked and launched this map as I truly believe understanding the full map is crucial for regulators, investors, entrepreneurs, and curious users alike!

As stablecoins grow into a core part of global finance, we expect continued innovation. For example, my work on the CXDR token (on canhav.io) aims to tie stablecoins directly to international trade needs by using a basket of currencies and high-quality collateral. This is because as I’ve conducted my research, I’ve realized that multi-currency, over-collateralized hybrid stablecoins will be especially useful in trade finance and global payments, where currency risk and settlement speed are paramount.

For readers interested in diving deeper, many of the projects mentioned above have active websites and documentation.

Whether you want to track stablecoin flows on Nansen, swap tokens on Curve, or use a stablecoin wallet to send money home, there’s a rich landscape to explore.

Lastly, if you’re a researcher or company interested in stablecoins and blockchain for trade, or if you want to learn more about CXDR, I’d love to hear from you. Please reach out via email at waz@canhav.com or visit www.canhav.io to discuss partnerships, research collaborations, or to get involved. The stablecoin ecosystem is complex but really interesting (in my opinion, at least!).